)

The following article is sponsored content in partnership with Spirit Telecom. Business News Australia does not give financial advice.

Ever since its founding Spirit Telecom Limited (ASX:ST1) has been a growth by acquisition story.

The company has taken advantage of opportunities where it can deliver custom designed cloud-based technology and internet solutions for high growth markets such as schools, hospitals, aged care and medium sized businesses.

In February, the group completed the acquisition of the Trident & Neptune Group (TBG), a transaction which was directly aligned with strengthening Spirit's share of its target markets.

The acquisition of TBG saw Spirit create a new business division called Trident IT Solutions, providing the group with opportunities to cross sell to the markets it has identified.

These types of clients are moving through a major generational technology change as they migrate to the cloud and require high speed internet and specialised tech services which Spirit can now provide nationally.

The rapidly changing environment that is being caused by the COVID-19 virus has presented Spirit with additional traction to drive an accelerated growth agenda through mergers and acquisitions.

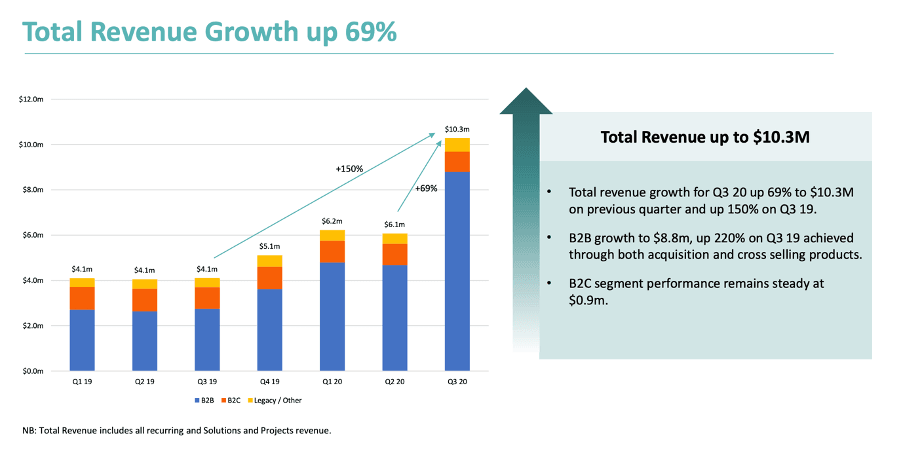

Acquisitions over the last 12 months, including TGB, have already made a significant positive impact on Spirit's revenue.

There has also been a significant uptick in gross profit over the last 12 months, increasing by approximately 50 per cent from $5.9 million in the first half of FY19 to $8.9 million in the first half of FY20.

Commenting on recent developments and the group's strategy going forward, Spirit's managing director Sol Lukatsky says now is a transformational period for Spirit.

"Through the acquisition of these businesses, Spirit will build and strengthen cloud, security, data and managed IT services capabilities whilst providing entry into target growth verticals including schools, health (hospitals) and aged care," says Lukatsky.

''The existing Spirit information technology and telecommunications division will continue to focus on the SMB (small to medium sized businesses) sector with the new Trident IT Solutions Division targeting higher value complex segments."

Acquisitions offer improved industry positioning and increased revenues

Not only do the acquisitions provide strategic advantages, but they will offer a significant boost to Spirit's revenue and earnings.

The company is currently focused on acquiring cashflow positive businesses that have a core customer base with a low probability of customer default sectors such as education and healthcare fit this profile.

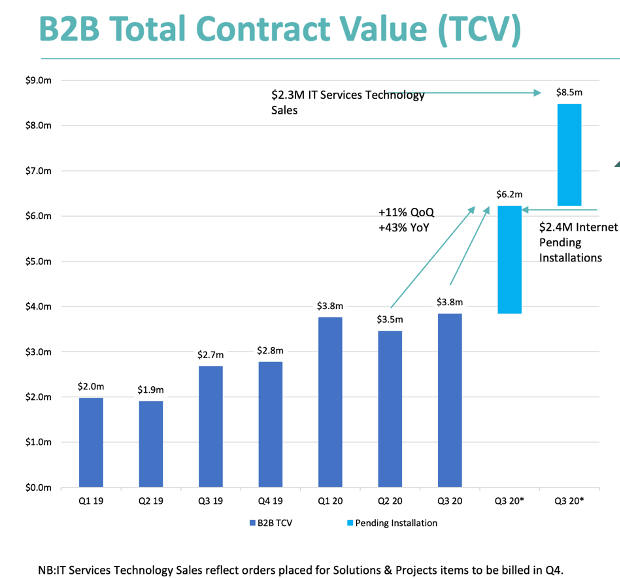

TGB generated combined revenue of $34 million in FY19, which is a welcome boost to total contract values (TCV) over the coming months.

TCV numbers are already strong at $3.8 million for the quarter, up 11 per cent on Q2 and 43 per cent to Q2 2019. Further, Total Data and IT services including pending installations valued at $2.4 million for IT services and $2.3 million for technology sales, total $8.5 million for Q3 2020.

The uplift in TCV is attributed to B2B telco sales and managed services, as well as maintenance of its average revenue per user (ARPU) value and contract length.

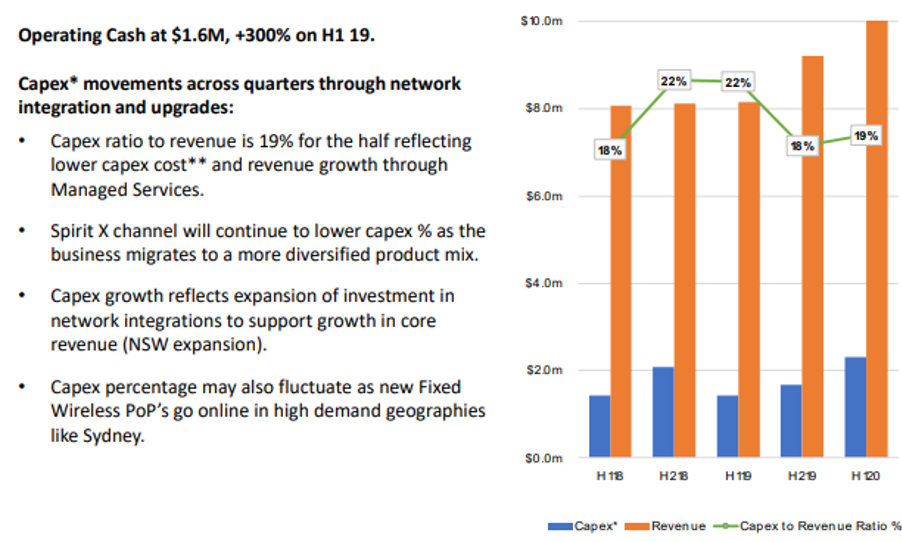

It is also worth noting that capital expenditure has also been reduced, in line with Spirit's strategy to move to cash flow positive status. The Trident acquisition (along with the rollout of Spirit-X, the company's telco digital sales platform) is an important element of this as the company continues to migrate to a more diversified product mix.

Management's ability to negotiate value adding acquisitions should come as no surprise given that the group integrated four new businesses in 2019, spanning the sales, marketing and billing areas.

Likewise, Spirit is demonstrating its ability to optimise the earnings and strategic value offered by these businesses.

The aggregation of new businesses under the one banner is set to continue with management recently flagging that it is conducting due diligence regarding potential acquisitions.

The group also recently expanded its debt facility to $10.9 million, extending a further $2.9 million over the past two months.

This, along with proceeds from a recent $9.2 million capital raising, will assist in funding future acquisitions in the MSP and Telco space.

Funds will also be used to expand Spirit X which generated 3,200 service qualifications in its first three months of operation across the third quarter of 2020.

Growth accelerates in March quarter

While it is one thing to make acquisitions, it is another to fully capitalise on the benefits of increased revenues and improved efficiencies while maximising earnings.

Even larger companies have bitten off more than they can chew, with some failing to successfully integrate acquisitions.

However, Spirit Telecom has demonstrated its ability to realise improvements at all levels.

This was particularly evident in its March quarterly market update, released in mid-April 2020.

The graph below demonstrates the nominal increase in capital expenditure compared with significant increases in revenues that have been achieved over the last two years.

Notably, capital expenditure in the second half of 2018 is broadly in line with the first half of 2020, but during that period the company has increased revenues by about 25%.

Consensus forecasts point to substantial share price upside

When companies are growing at this pace and it is difficult to forecast the quantum of upcoming transactions on the merger and acquisition front, it can be difficult to arrive at a valuation.

As a guide, consensus forecasts for 2021 are based on revenues of $46 million with EBITDA expected to be the vicinity of $3.2 million, representing earnings per share of 0.9 cents.

However, it is worth noting that management expects to be generating revenues at a run rate of circa $80 million per annum by the end of calendar year 2021.

Consequently, there could be a significant upside to consensus forecasts.

Notwithstanding the potential for earnings upgrades, the consensus share price target is 30 cents, implying share price upside of 100% based on Spirit's opening price of 15 cents on 11 May 2020.

Never miss a news update, subscribe here. Follow us on Facebook, LinkedIn, Instagram and Twitter.

Business News Australia

Get our daily business news

Sign up to our free email news updates.

)

)

)

)

)