)

FALLING freight volumes and asset write-offs hurt Aurizon in FY16 (ASX: AZJ), and the railway operator will cut hundreds of staff in the coming year to improve the performance of the business.

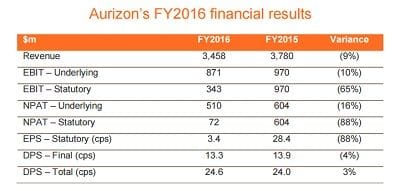

In full-year results released today, the company reported Underlying EBIT was down 10 per cent to $871 million, while underlying profit sank 16 per cent to $510 million. Revenue declined 9 per cent to $3.46 billion. Statutory NPAT reduced by 88 per cent compared to the previous year, due to $528 million in asset impairments; the largest being a $226 million investment in Aquila Resources, in addition to $177 million in rolling stock and $125 million in other strategic projects.

In the full report, Chairman Tim Poole says the asset impairments are disappointing.

"We need to improve our approach to capital allocation in the future," he says.

However, to put the profit result in perspective, the company in FY15 reported a 139 per cent increase in profit after the FY14 profit was impacted by a $69 million redundancy program and $317 million in asset impairments.

Aurizon bought and cancelled $301 million in its own shares in FY16, but has stopped the buyback unfinished to "manage near term balance sheet capacity".

AZJ will continue to reduce staff and restructure its management and it said today that most profit growth in the coming year will come from the "transformational benefits".

It will cut 300 jobs this year - 120 in management and 180 in train crew, yard operations and maintenance and will reduce direct reports to the CEO from seven to five. Since listing in 2010, the company has reportedly cut 3,000 jobs.

Total above rail volumes were down 4 per cent to 270.9mt in FY16. Based on current market conditions, rail haulage is expected to remain flat in the range of 255mt 275mt during FY17, with coal in the range of 200-212mt.

Aurizon Managing Director and CEO, Lance Hockridge, says pressure on volumes and revenue, particularly in freight, created a challenging year.

"However, we have seen a stabilisation in coal volumes in the second half, with relatively resilient earnings for the year in a lower volume environment," he says.

Even as it released the full-year result, the company announced a new haulage contract to transport 800,000 tpa of coal per year from Wollongong Coal's Wongawilli Colliery to Port Kembla Coal Terminal for Indian conglomerate Jindal Steel and Power Limited.

Transformation will be the major driver of earnings growth in FY17, with $131 million delivered this year, along with an uplift in EBIT from the below-rail network business.

The company is targeting an additional $250 million in cost reductions and productivity improvements to take $380 million out of its cost base for the three years to FY18.

That is part of a five-year plan to reduce costs by $630 million between FY14 and FY18.

"A number of substantial initiatives have been recently commenced including a new regional model for operations, improved alignment of train crew and maintenance workers to long term demand, the outsourcing of non-core maintenance activities, and the continued consolidation of corporate support functions," says Hockridge.

In FY17 the company expects to increase underlying EBIT to between $900 million and $950 million, excluding $100 million in restructuring costs.

AZJ is trading down 5.80 per cent this morning, at $4.71 per share, making it one of the worst performers on the ASX this morning.

Get our daily business news

Sign up to our free email news updates.

)

)

)

)

)